Stories

Hermès – Strategy Insights Of Luxury Brand

Hermès, a French fashion luxury goods manufacturer, has been ranked consistently as world’s most valuable luxury brand and one of the best global brands. Hermès, which is also known as Hermès International or Hermès Paris, has maintained an iconic status in the luxury market with products ranging from leather goods, perfume and lifestyle accessories to watches.

In 2018, the Company’s net profit rose to 1.41 billion euros, a 16 % increase from 1.22 billion euros in 2017. Fifty percent of the Company’s profits came from the brand’s leather goods and saddlery products. With competitors like LVMH and Richemont in the luxury business, Hermès still enjoys the top position in the market because of its exquisite craftsmanship and eye for detail through the entire manufacturing process.

History

Founded in the year 1837 by Thierry Hermès, the Company’s initial purpose was to build saddles, bridles and other leather riding gear for European nobility. After taking over the Company from his father, Charles-Émile moved the Company to 24 Rue Du Faubourg Saint-Honore in Paris in the 20th century. This remains the global headquarters of Hermès till date.

Through the generations, the Company slowly expanded from selling leather saddles to other products. The Company started selling “Haut à Courroies” bags in 1900, which were used by riders to carry saddles in it. The Company introduced its first leather handbag in 1922, a product which has played a significant role in increasing the popularity of Hermès in the global market.

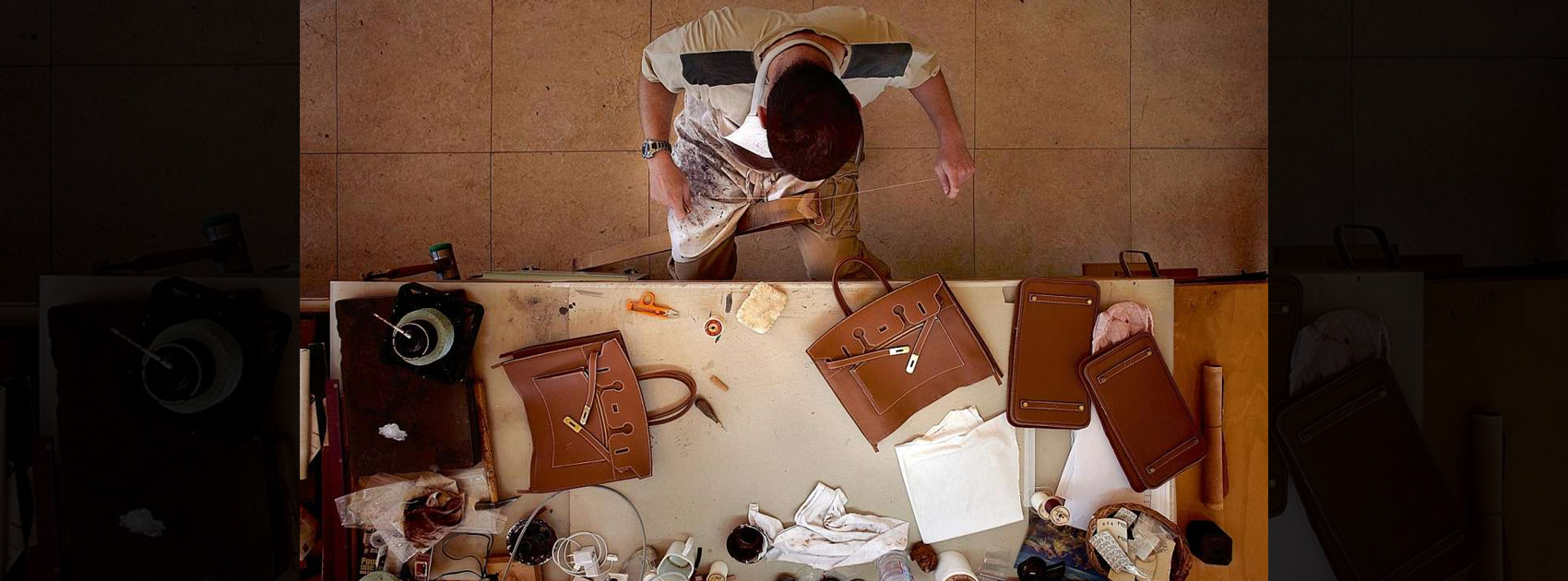

Strategy

Hermès has a unique strategy in place to ensure it retains its position on top in the market. Hermès is very strict about the traditional way of manufacturing and rejects any form of mass production. Every product produced by the Company is handmade by craftsmen who are trained for a period of two to three years. According to the Company, every product is made from beginning to end by a single person to preserve the product quality and uniqueness.

Jean Louis Dumas, the chairman of Hermès from 1978 to 2006, told Vanity Fair, “We don’t have a policy of image; we have a policy of product.” Hermès has always claimed, it values creativity more than anything and to this day, maintains a deep connection to its French identity. Most of Hermès’ products are manufactured in France and 60 % of the Company’s workshops are located in different parts of the Country.

Another strategy the Company uses is giving a sense of exclusivity. In order to do so, Hermès uses the “Limited Edition” strategy and releases only a handful of products at a time. The Birkin bag, created by Hermès for Jane Birkin in 1982, remains the most popular product by the Company. One of the reasons behind this is the brand’s strategy to make the customer wait for a few months or a year after making an order. The cost of each Birkin bag ranges from 7,000 USD to 300,000 USD. Every Birkin bag is made of crocodile skin and has exquisite handiwork by a single craftsman.

The brand continuously collaborates with other ultra luxury brands to maintain its reputation in the market. Hermès has collaborated with luxury designers like John Lobb, Saint Louis as well as tech mogul Apple. Each collaboration brought the Company media attention and skyrocketed its brand value and sales.

Keeping it in the family

For the last 180 years, since the founding of Hermès, it has been run exclusively by the Hermès family. Currently, the brand is managed by Axel Dumas (6th generation,) who is the sole manager of the Company. The Company maintains its independence and uniqueness by keeping the control within the family.

Even though Hermès is 180 years old, it still maintains an ultra luxury status because of its ability to evolve by maintaining a perfect balance between tradition and modernity. With its clever strategy of exclusivity, controlled marketing and limited edition, Hermès is able to engage potential and wealthy clients, which ensures continuous profits and growth of the Company.

Emerging Startup Stories

Suki: This Startup Wants To Transform Healthcare With Its Artificial Intelligence Tool

Meta’s AI Assistant, Meta AI: Friend or Foe for Searching Giants?

Discover Kheyti, The Startup Changing The Lives of Farmers In India